This September 2023, the Student Loan Plan 5 launched for new university and college starters.

There are a lot of questions about what these changes will mean. For many, there won’t be any changes at all - those who started university or college between September 1st, 2012 and July 31st, 2023, will still be on the Student Loan Plan 2.

But, if you started university or college on or after August 1, 2023, then you’ll be on the new Plan 5.

So, let’s dive into what that means for you and your finances. 🧑🎓

What are the key changes to Plan 5?

First of all, you don’t have to pay anything just yet. You’ll only start repaying once you’re earning over the repayment threshold. If you’re earning over the threshold as soon as you leave university, you’ll start repaying the April after you finish or leave your course.

The two most important changes to the repayment plan are:

-

The income threshold for repayments has changed from £27,295 to £25,000

-

And the repayment write-off period (when the debt is written off) has extended from 30 years to 40 years

In a nutshell, if you’re on Plan 5, you’ll likely start paying your loan back earlier (due to the lower income threshold), and you’ll be paying it back for longer (due to the cut-off time).

So, here’s everything you need to know about Student Loan Plan 5 💰

You only repay once you start earning £25,000

Currently, students begin to repay their loans once their annual income has reached or exceeded £27,295, but that threshold has now changed to £25,000. If you earn less than £25,000, you don’t pay anything back.

You repay 9% of everything earned above £25,000

What you repay each month depends only on what you earn. The more you earn, the more you pay back. You also repay automatically through payroll, sort of like income tax (which is the same as previous loan plans).

At the end of the tax year, you can ask for a refund if:

- you paid more than what you actually owe

- your annual income is below the threshold amount

- you made repayments before you needed to

- your employer had you on the wrong repayment plan

The below chart shows the difference between Plan 2 monthly repayments and Plan 5 (data from HM Revenue & Customs):

Annual income (pre-tax) |

Plan 2 approx. monthly repayment |

Plan 5 approx. monthly repayment |

|

£25,000 |

£0 |

£0 |

|

£26,000 |

£0 |

£7 |

|

£28,000 |

£5 |

£22 |

|

£31,000 |

£27 |

£45 |

|

£33,000 |

£42 |

£60 |

You only start needing to repay the loan the April after you leave university or college

You don’t pay anything until after you’ve graduated or leave university or college. And Plan 5 repayment won’t begin until the April you finish or leave your course if you started in September 2023.

The loan is wiped after 40 years (or if you die) vs 30 years

Student loans in the UK have an expiry date - any money still owed after the deadline is cancelled and you no longer have an obligation to pay it back.

If you’re on Plan 2, your student loan gets wiped at 30 years. But now for Plan 5, it gets wiped after 40 years. This means you’ll be paying your loan back for longer.

And while it may sound grim, if you pass away, your loan (on any plan) does get wiped out. It does not get inherited by your beneficiaries (family).

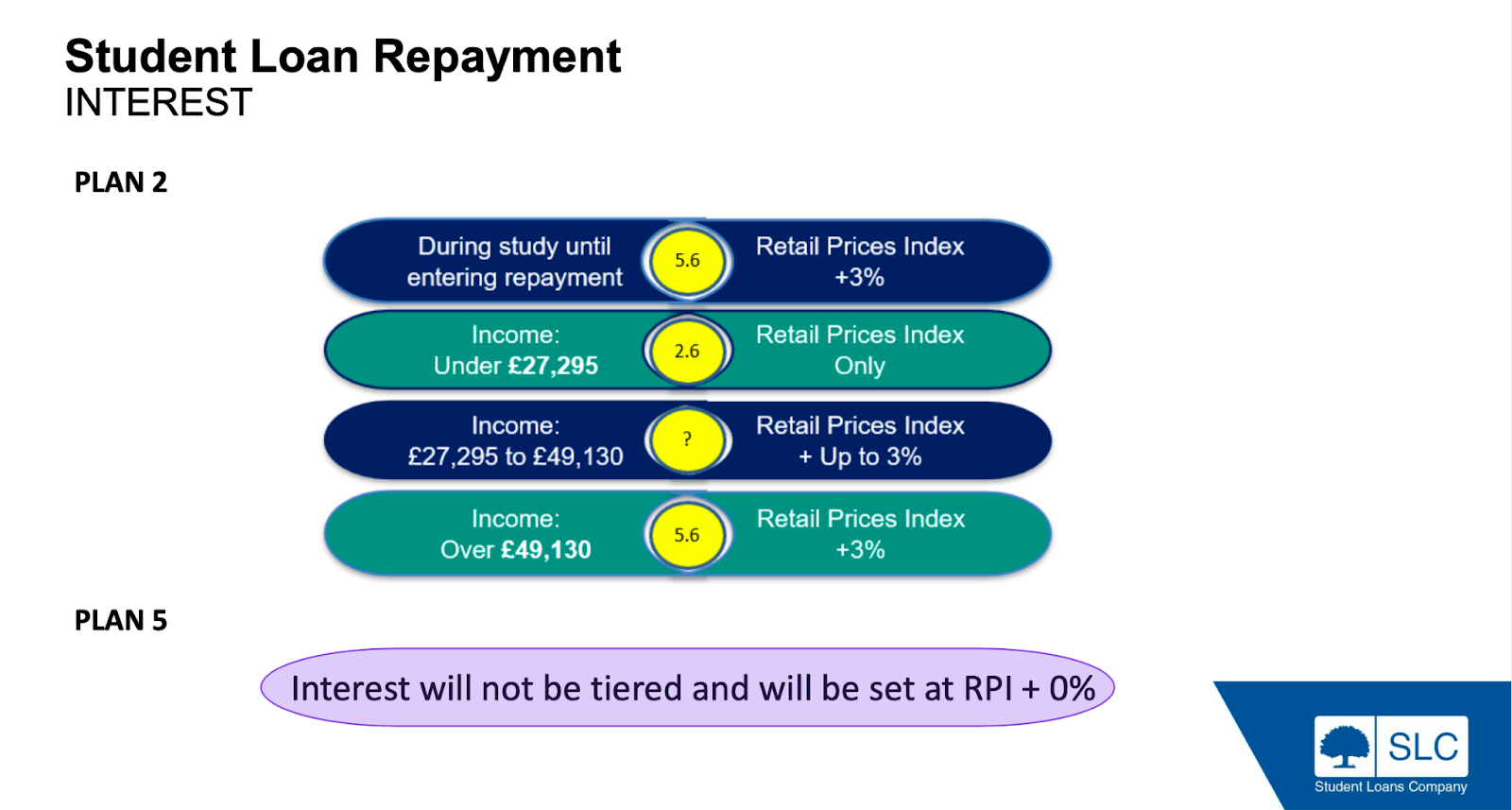

There’s no additional interest on Student Loan Plan 5

Plan 5 loans will be set at the Retail Price Index (RPI) rate of inflation - whereas Plan 2 loans were set at the RPI plus an additional 3% interest. So, for those on Plan 5, the amount you pay back will go up based on the value of the pound and the price of goods and services, but not based on additional interest.

The government has said they hope that with a lower interest rate, higher earners will be able to pay back more of their loan. They predict that the number of students who will pay back their loan will double from 23% to 52% as a result of these changes. This increases the monthly repayment burden a little on higher earners but reduces the total interest that a graduate will pay.

It’s also important to note the following:

-

Student loans do not go on your credit file

-

You still have to repay your loan if you move overseas

-

The more you earn, the more you repay each month, but the faster you’ll clear your debt

-

The less you earn the less you repay each month

-

If you never earn over the threshold, you never have to repay the loan

Why the change? 🤔

These changes, the government has said, are intended to make the fees ‘fairer for taxpayers and for students’. Why taxpayers? Because debt that isn’t paid back by students becomes the responsibility of the nation’s taxpayers.

The government also claims that this is done to make sure that those on the new Plan 5 ‘will not repay more than they originally borrowed over the lifetime of their loans, when adjusted for inflation.’

However, according to Martin Lewis (Money Saving Expert),

So while some of these changes are good - there’s no additional interest on the student loan on top of the RPI interest - overall, it benefits higher earners who may pay higher amounts but for a shorter period of time. Whereas lower-to-middle-earners, in the end, will end up paying more in small payments over a longer period of time.

What if I can’t repay my student loan?

Paying your student loan back is mandatory and the SLC have the right to take legal action to recover your debt. Under Plan 5, loans will be wiped out after 40 years - but you’ll be paying it back automatically through payroll up until that point.

So, depending on your income, you may be paying an additional 9% tax on your income that’s over the threshold for some, or even most, of your working life.

That being said, learning to manage your finances early on and while you’re in university and college can help you budget with your repayments in mind once you’re working. Blackbullion has lots of resources for money management, debt, investing and saving and more.